")

Studying processes allows for a comprehensive understanding of sectors. This is the premise behind the Quarterly Thermometer of the State of the Organic Sector (QTSOS). In the edition corresponding to the second quarter of 2025 (April–June), companies with varied profiles participated, ensuring a representative and balanced sample of the sector.

In the data collected in the QTSOS for Q2 2025, the sample is made up of 39% of companies engaged in marketing, 20% in distribution, and 41% focused on manufacturing. In terms of the size of the participating companies, 50% have fewer than 10 employees, 25% have between 10 and 50 employees, and 25% are companies with more than 50 employees. Finally, in terms of the production sectors represented within the organic field, companies from the food, natural cosmetics, food supplements, and household and cleaning products sectors participated.

Key thermometer results

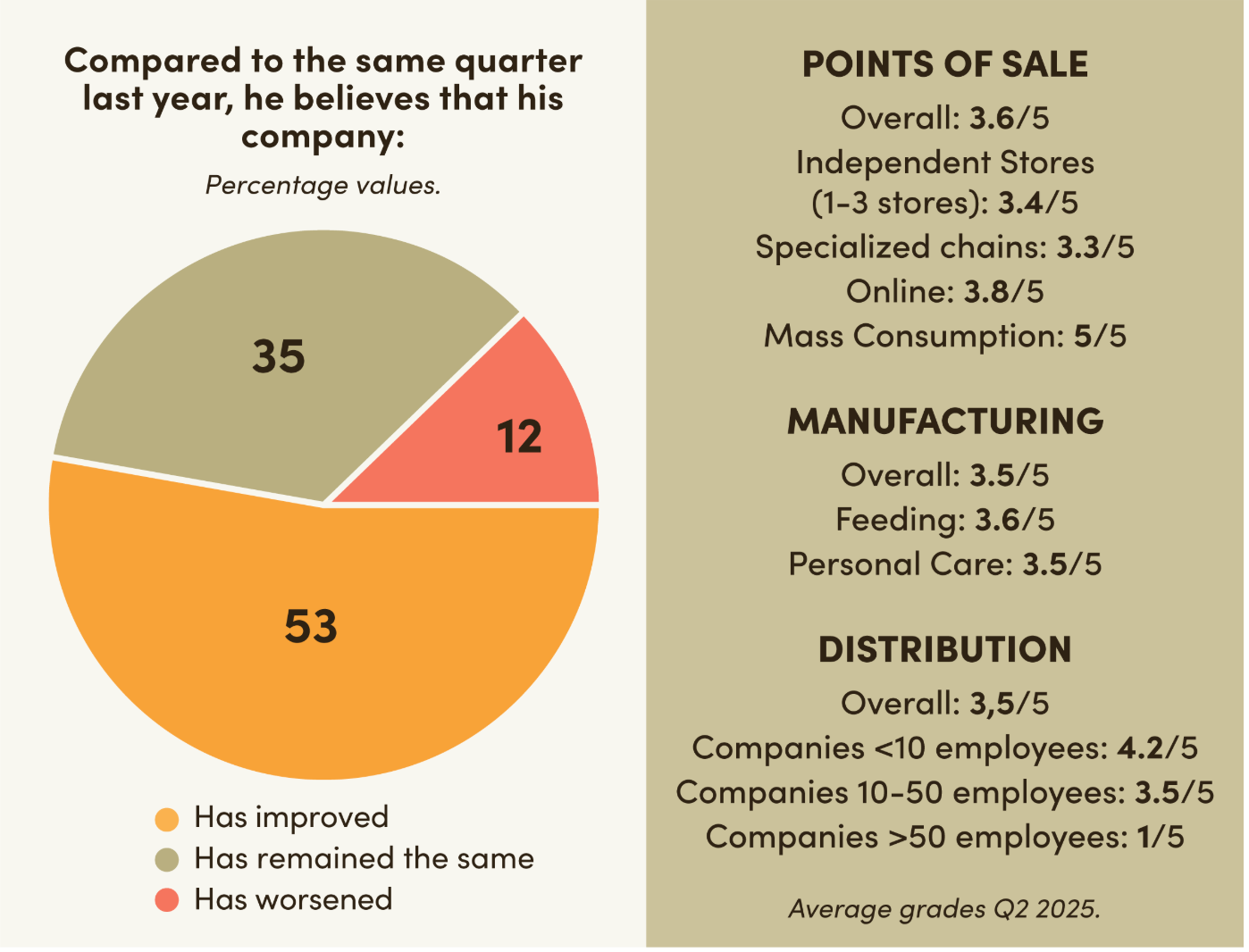

The average rating for the organic sector in the second quarter of 2025 is 3.5 out of 5. 53% of companies say their situation has improved compared to the same period last year, 35% say it has remained stable, and only 12% indicate a negative trend.

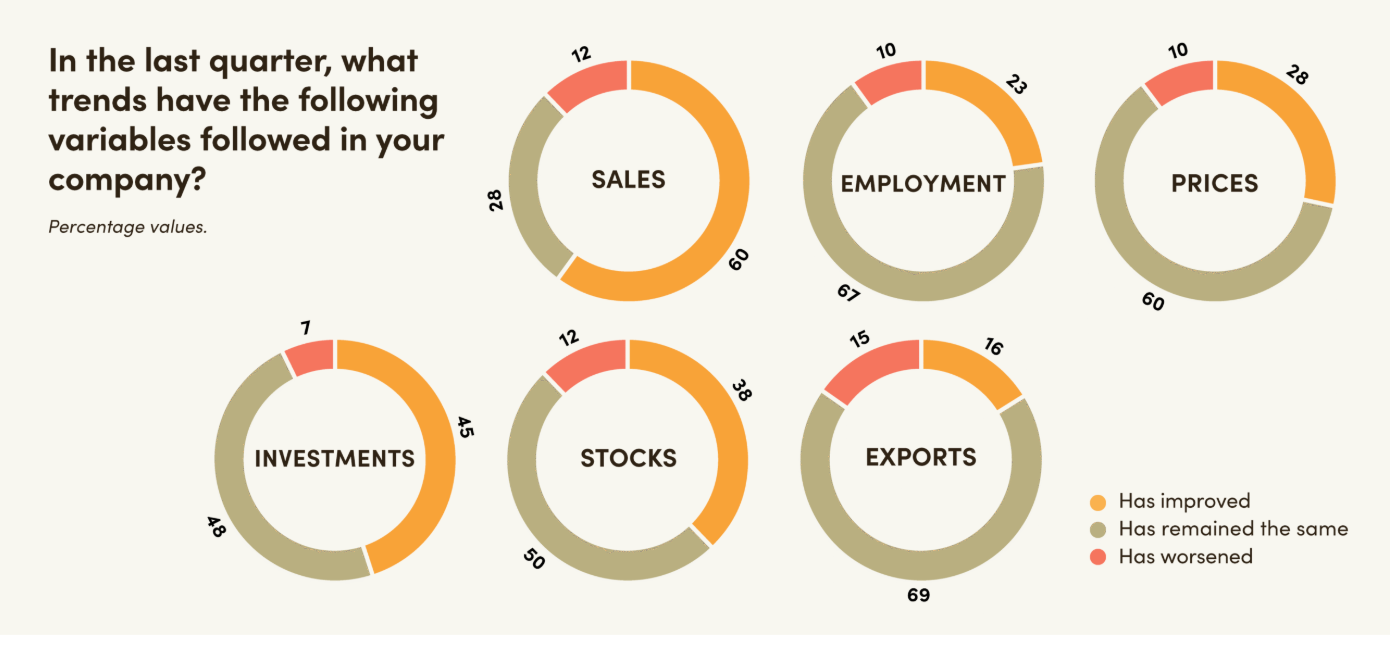

When analysing the results by variable, the following trends can be observed:

- Sales: 60% of companies indicate that they have experienced an increase in the last quarter, while 28% report stability and another 12% mention a decline.

- Employment: 23% of companies have increased their number of employees, 60% have maintained their workforce, and only 10% have reduced their staff.

- Prices: 62% of companies have maintained their prices, 28% have increased them moderately, and only 10% have managed to lower them.

- Investments: 45% of companies increased their investment, 48% maintained it, and 7% reduced it.

- Stocks: in terms of stocks, 50% of companies maintained levels similar to those of previous periods, 38% increased them, and 12% reduced them.

- Exports: the sector reaffirms its export-oriented nature, with 69% of companies maintaining their export levels, 16% increasing them and 15% decreasing them.

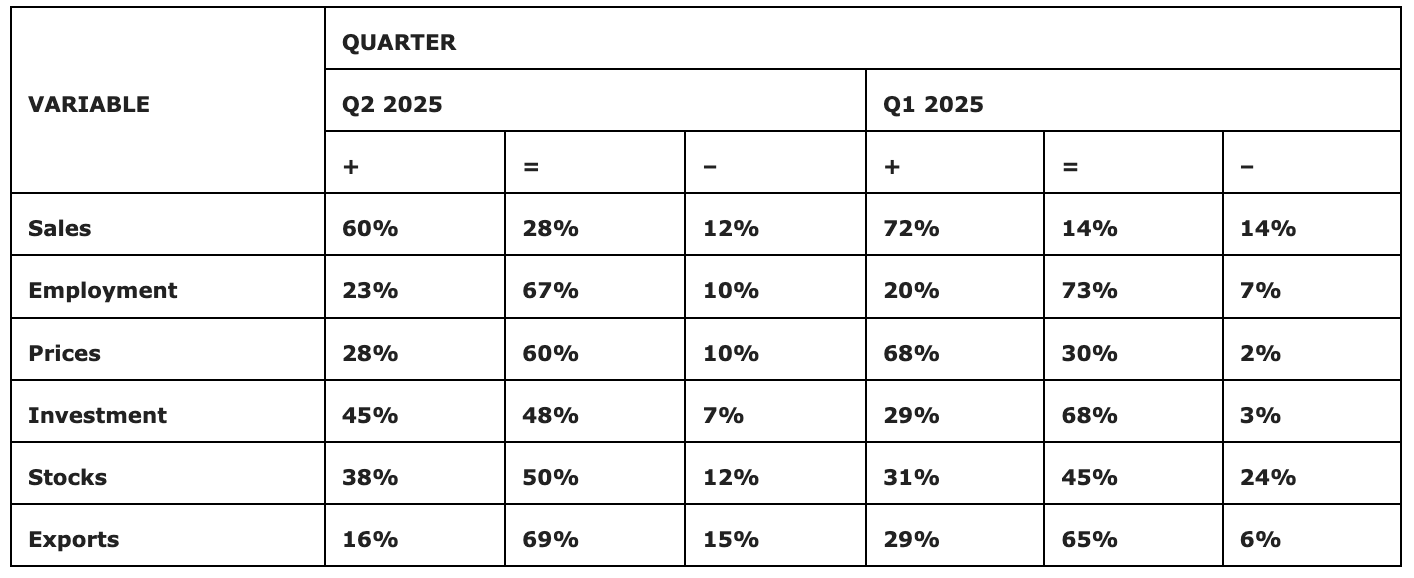

If we compare them with the data obtained in the first quarter of 2025 (Q1).

Table 1: Comparison of the percentages of the variables between Q1 2025 and Q2 2025

Source: Prepared by the authors using data from QTSOS Q2 and Q1 2025.

We can observe the following relevant dynamics:

- Prices stabilised after a general increase in Q1, with 68% of companies increasing them. In Q2, most companies are maintaining prices, and a higher percentage are lowering them.

- Sales indicators remain strong, although the percentage of companies reporting an increase is lower, falling from 72% to 60%. However, we can see that the percentage of companies maintaining their sales has increased, while fewer companies are reporting lower sales rates.

- This Q2 shows a significant increase in investments, with 45% of companies increasing them, compared to 29% in the previous quarter. This means that, during the months of April to June, 93% of the companies surveyed increased or maintained their invested resources, demonstrating confidence in the organic market and in their ability to increase their profitability.

Prices stabilise: after a general increase in Q1 2025, in Q2 most companies are maintaining prices

Perceptions of the sector as a whole

In general terms, companies rated the last quarter in sectoral terms with an average score of 3.6 out of 5. This result is very similar to the rating given to their own companies, which was 3.5 out of 5, and slightly higher than in Q1, when the average was 3.4 out of 5.

When comparing the quarter with the same period last year, 95% believe that the situation has improved or remained stable—45% and 50%, respectively—while only 5% perceive a deterioration in the sector as a whole.

Future prospects

In terms of future projections, the Thermometer reflects optimism, with 40% believing that their situation will improve over the next quarter, the same percentage expecting it to remain unchanged, and 20% express doubts or anticipate a decline, as Q3 includes the summer months, when the habits and priorities of eco-conscious customers are altered.

Regarding how the sector as a whole is expected to evolve, 38% of companies are confident that it will improve, 42% believe it will remain unchanged, and 17% think it will worsen or express uncertainty about the sector’s development.

Results by production sector

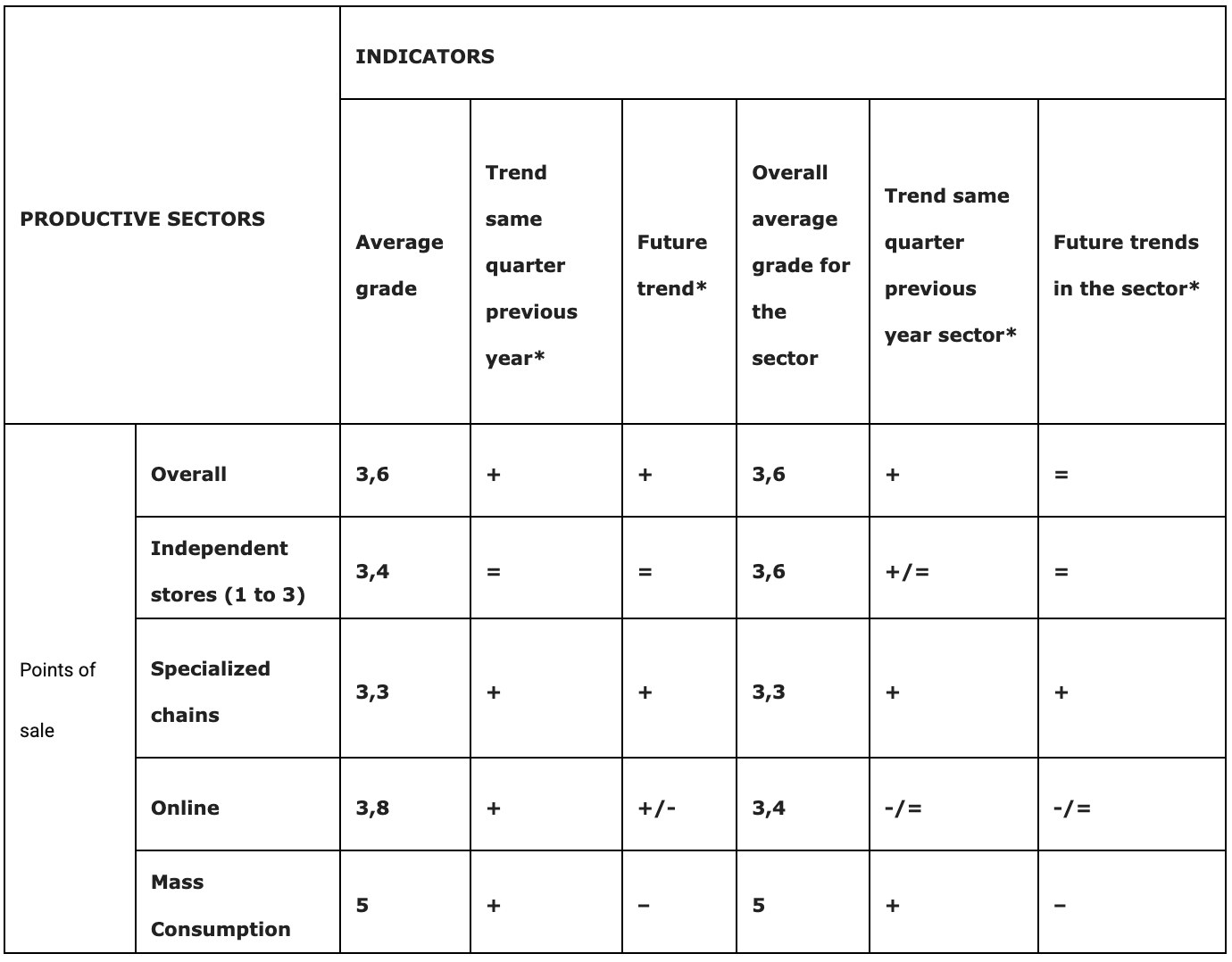

Points of sale

If we analyse all points of sale (shops, chains, online stores and mass-market retailers), we see that the average score is 3.6 out of 5. This is very similar to the score for Q1, which was 3.7 out of 5.

In terms of trends compared to the same quarter last year, it is noteworthy that no company reported that its situation has worsened compared to Q2 2024. In this regard, 61% of points of sale say that their company has improved and 39% say that it has remained at similar levels. As for future prospects for Q3, the trend is optimistic: 39% expect their company to improve, 33% anticipate that it will remain stable and 28% foresee uncertainty or a potential deterioration.

As for the organic sector in general, retailers give it an average score of 3.6, which is the same score they give their own companies. Compared to the same period in 2024, 50% of retailers believe that the sector has improved, while 45% believe that it has remained stable, and 5% perceive a deterioration compared to the second quarter of last year. Looking ahead to the next quarter, expectations for the sector’s performance are mostly stable: 45% think the situation will remain unchanged, 28% expect an improvement, and 27% anticipate either a deterioration or uncertainty.

Table 2: Results broken down by points of sale

Tabella 2: Risultati suddivisi per punti vendita

*(+), (=), or (-) depending on the majority trend. (+) indicates: it has improved, (=) indicates: it has stayed the same, and (-) indicates: it has worsened. Source: Prepared by the authors using data from the QTSQS Q2 2025 survey.

We can observe the following key observations:

- The average quarterly score for points of sale is particularly high for mass-market outlets, i.e. retail outlets offering conventional and organic products, which clearly harms businesses specialising in certified products.

- Retail outlets are particularly concerned about changing habits during the holiday period and are uncertain about sales.

- All retail outlets report either increasing or stable sales trends compared to the same quarter in 2024, demonstrating positive momentum in the growth of the organic sector market.

Looking ahead to the next quarter, expectations regarding the sector’s performance remain mostly stable.

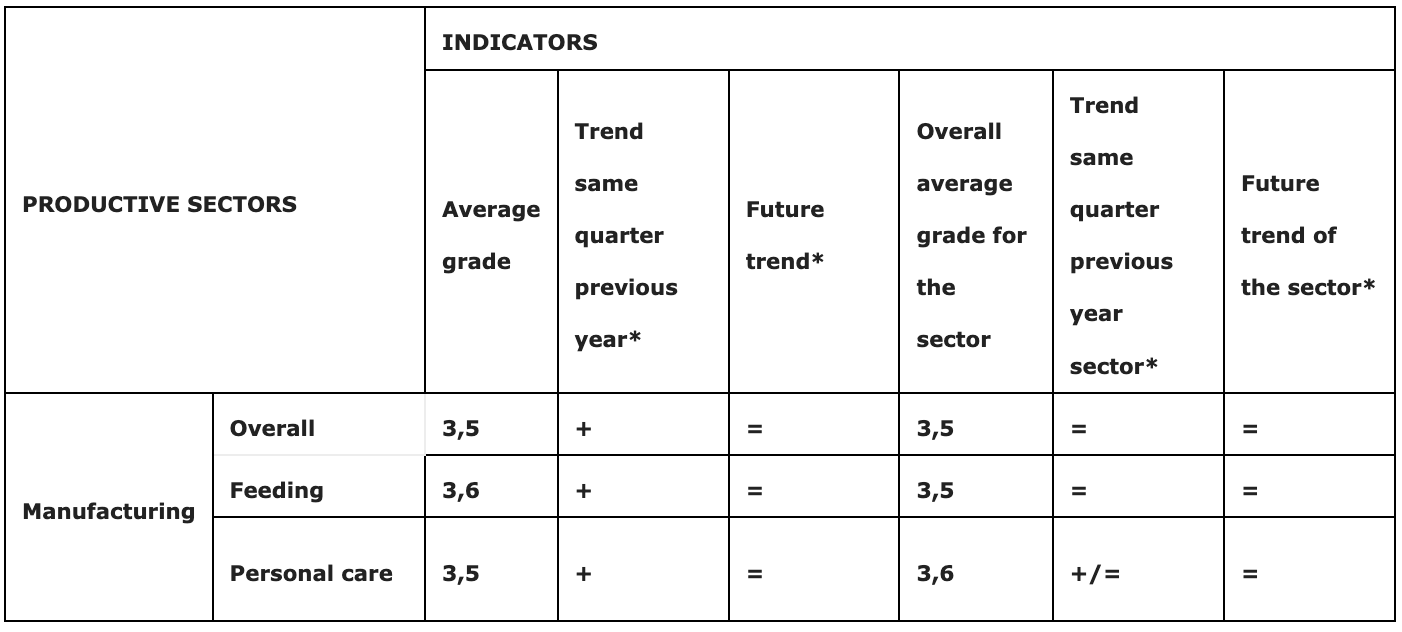

Manufacturing

Companies engaged in the manufacture of organic products during the second quarter of 2025 rated their performance with an average score of 3.5, representing a slight decline compared to the first quarter of 2025, when they achieved a score of 3.8 out of 5.

Compared to the same quarter of the previous year (Q2 2024), producers show a significant improvement: 50% say they have improved, 28% say they have remained the same, and 22% say their situation has worsened. Looking ahead to Q3 2025, 50% estimate that their results will remain stable, 28% are confident of an improvement, and 22% believe that their production will decline.

When analysing how manufacturing perceives the sector as a whole, we observe that the average score given is 3.5, the same rating as for its production area. On the other hand, 45% consider that the sector has improved compared to the same quarter in 2024, while 50% believe that it has remained unchanged and 5% perceive a decline. Finally, when asked about their expectations for the third quarter of 2025, the forecasts are mostly optimistic: 33% anticipate growth in the sector, 39% believe it will remain stable, and 28% foresee a decline.

If we break down manufacturing by production area, we obtain the following information:

Table 3: Broken down results of manufacturing companies according to their production area

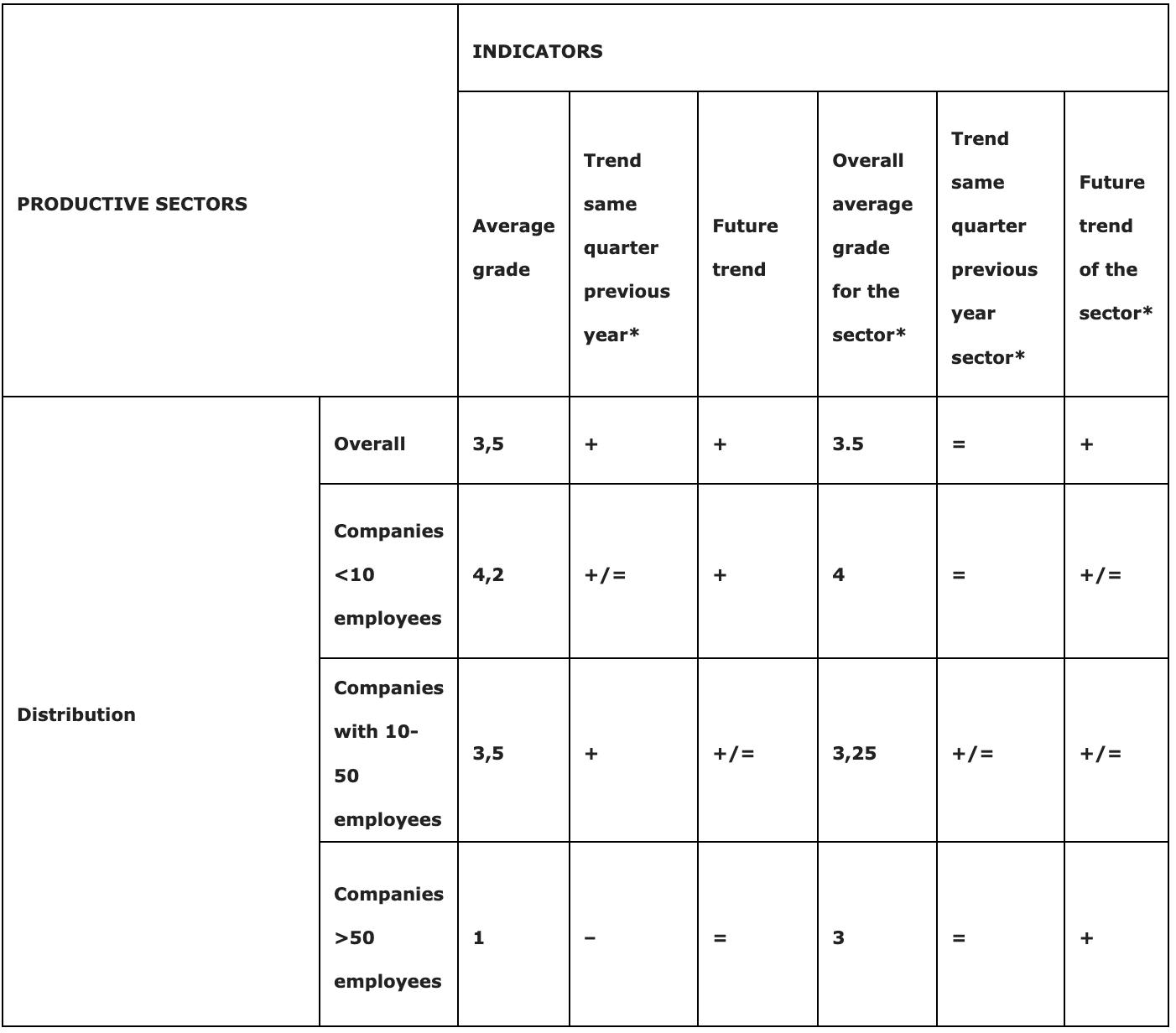

Distribution

With regard to organic product distributors, the average rating for the quarter stands at 3.5 out of 5, slightly below the previous quarter, when it was 3.7. However, when compared to the same period in 2024, the trend is positive: 56% indicate improvement, 22% that it has remained stable, and 22% say their situation has has worsened. Looking ahead to Q3, 56% expect an improvement, 33% anticipate stability, and 11% anticipate a worsening of their situation.

From a sector-wide perspective, companies give an average score of 3.5 out of 5. Compared to the first quarter of 2024, 67% consider that it has remained stable and 33% perceive an improvement in the sector. As for forecasts for the next quarter, 56% anticipate growth, compared to 44% who estimate that there will be no change.

If we break down the distribution according to size, we obtain the following information:

Table 4: Results broken down by distribution companies according to their size

Key points:

- The quarter has been marked by highly uneven dynamics depending on the size of the companies surveyed, with poor results for companies with more than 50 employees, which report lower rates than in the same quarter of the previous year.

- Distribution companies with fewer employees are the ones that have posted the best quarterly results, both in terms of average scores and future prospects, demonstrating their commitment and confidence in continued growth with a highly optimistic outlook.

As a summary of the productive sectors as a whole.

Sectorial challenges

When asked about sectoral challenges, the companies surveyed reflected on various issues. On the one hand, the difficulty of maintaining competitive prices in a context of rising production costs and the increase in large supermarkets and online stores selling organic products. Democratising consumption without compromising the quality and sustainable values that characterise it is particularly difficult and would require greater public support.

On the other hand, tackling greenwashing by emphasising that organic products are not only an environmentally responsible choice, but also the healthiest and most sustainable alternative for personal well-being and the planet, is also one of the major common challenges. In short, preserving and increasing market share in order to continue growing, by spreading the narrative of sustainability and health, is currently the most widely shared concern in the sector.

All data is managed by Bio Eco Actual, without publishing identifying information and treated anonymously and in aggregate form. To find out more or contribute data to the Quarterly Barometer of the Organic Sector, please contact: marketing@bioecoactual.com

Author: Gemma Isern Castells, Political Scientist, Master in International Relations, Security and Development