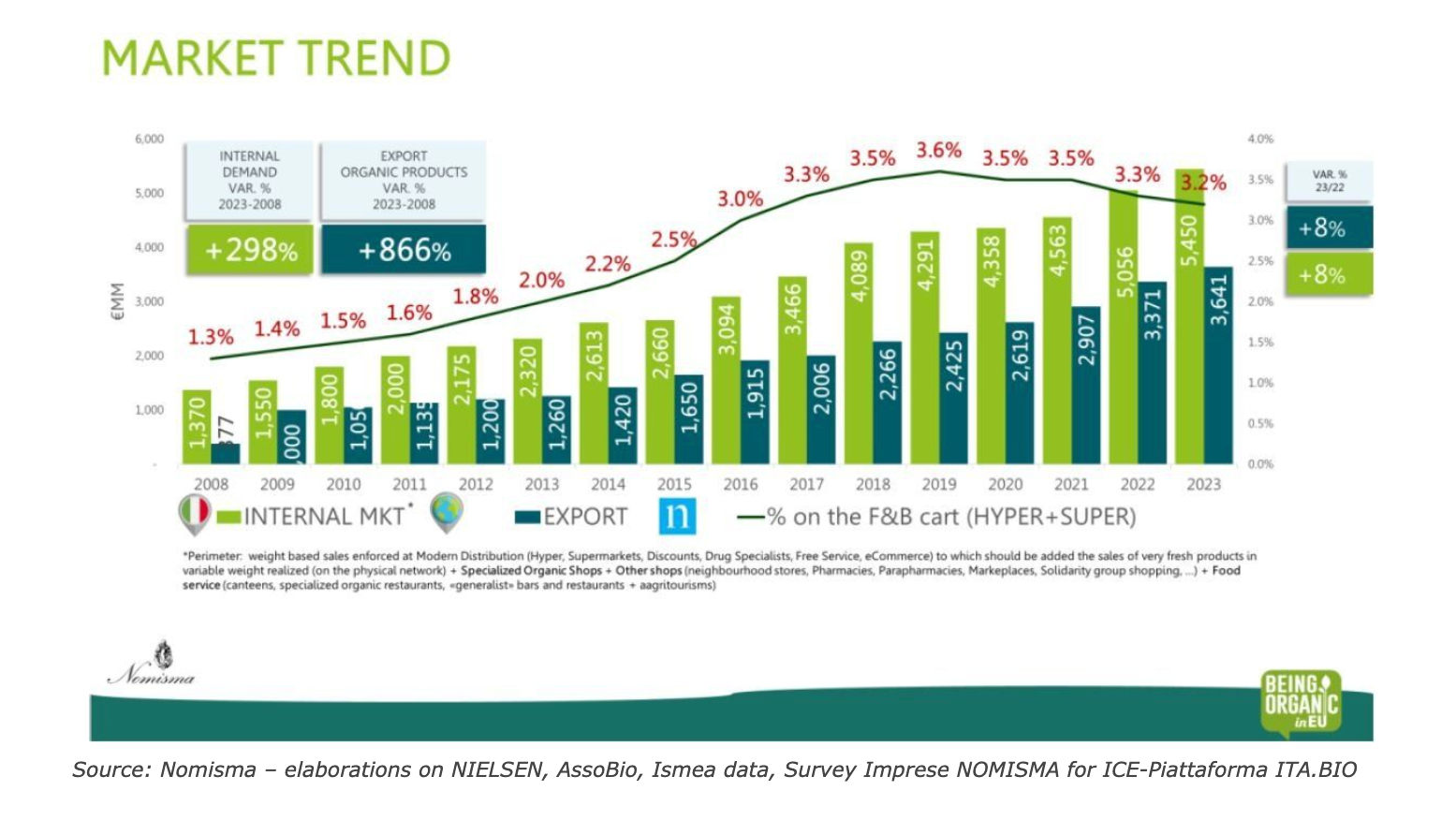

Nomisma presents at BIOFACH 2024 the results of the market survey carried out as part of the Being Organic in Eu project, managed by FederBio in partnership with Naturland DE and co-financed by the EU under EU Reg. n.1144/2014. The survey shows that the organic sector maintains a key role in the agri-food supply chain with a domestic market (domestic consumption and away-from-home consumption) nearly €5.4 billion euros and exports of Made in Italy organic products reaching 3.6 billion.

Italians paying more and more attention to sustainable food choices

In Italy, inflation has been gradually slowing down: in 2023, prices rose 5.7 %, down from 8.1% in 2022 but still having a significant impact on Italian household (the additional cost inflation burden for a family with two children was at least €1,600, of which more than €700 related to food). Despite the deceleration in price growth, this situation has led Italian consumers to adopt strategies to protect purchasing power.

In this context, 9 out of 10 Italians adopted strategies in order to deal with rising food costs: specifically, 71% stopped purchasing superfluous products, 64% did their shopping by looking primarily at special offers, while 6 out of 10 Italians purchased private label products. Despite the difficulties which characterized the past year, in 2024 Italians’ intentions to spend more on household food consumption appear to be improving: the percentage of those who intend to increase the quantity consumed (16% of the total) in fact exceeds that of those who intend to reduce consumption (11%), considering that the same difference was -1 percentage point in the monitoring conducted in August 2023.

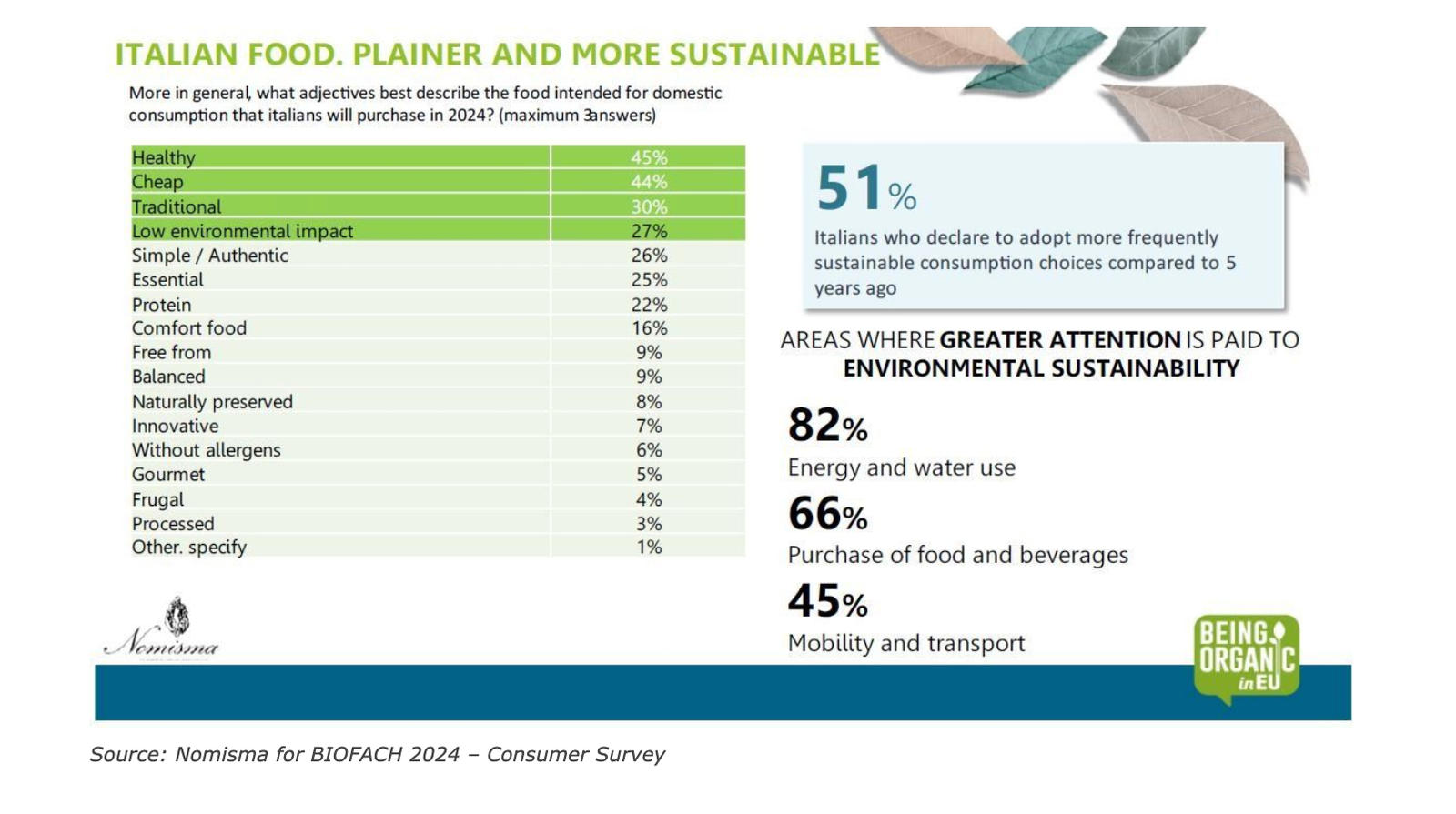

The Italian food shopping choices in 2024 must not only be affordable, but also ensure certain basic requirements: to be healthy, traditional, environmentally friendly, easy to use and essential. A further sign that a turnaround is under way in the Italian shopping cart is the fact that fruits and vegetables, after some declines reported in the summer, are now among the products with the highest increases in sales.

In this complex scenario, attention to sustainability and the environment has become a key determinant of purchasing behaviors. In this regard, 1 out of 2 Italians stated that they have been more frequently adopting sustainable consumption choices in the last 5 years.

These habits reflect a greater commitment to reducing the climate impact of one’s actions, including putting items in the shopping cart: indeed, 2 out of 3 Italians said they pay more attention to buying food and beverage products with sustainability features.

Italian organic market size

Cultivated surfaces and organic operators

With more than 2 million hectares under cultivation, Italy is a leader in the organic sector: it has the highest percentage of organic land of the total cultivated area–19% compared to 11% in Germany and Spain, and 10% in France, and it holds the lead in the EU for the number of organic operators.

Italian organic market size

In 2023, organic food sales in the domestic market (domestic consumption and away-from- home consumption) nearly reached €5.4 billion. Away-from-home consumption also drove market growth in 2023 with an increase of +18% compared to 2022 and a value of nearly €1.3 billion. After last year’s slight decline, at-home consumption registered a positive increase of +5%.

Compared to 2022, sales through the specialized retail channel started to grow again, rising +4.5%, while sales through large scale retail increased in value by 5% with other channels increasing by 6% (including direct sales carried out in markets and farms, solidarity buying groups, pharmacies, para-pharmacies and herbalist shops…).

The impact of modern distribution in the Italian consumer market

Modern Distribution is confirmed as the main purchasing channel for Italian consumers: in 2023, organic food purchasesin odern Distribution stood at €2.1 billion (omnichannel perimeter, source: Nielsen IQ). odern Distribution remains the main purchasing channel for organic food by Italians both in terms of its role compared to other purchasing channels (accounting for 58% of total sales related to Italian household consumption) and in terms of product selection (private label now account for 47.5% of the value of sales carried by modern distribution).

Within Grocery Retailing, in 2023, the Hypermarkets + Supermarkets channel accounted for about €1.5 billion in organic product sales (perimeter: fixed-weight packaged products; source: Nielsen), up since 2022.

If we look at the most sold organic products, we find eggs (+9.7%), crackers (+4.4%) and fruit-based spreads and ams (+6.2%). Among other products that registered an increase in value sales are preserved fruits which grew +33.6% and bananas +25.5%.

Exports of Italian organic products

The trade balance for Italian organic products is positive, with exportsreaching €3.6 billion in 2023, marking a growth of +8%, in line with the trend of agri-food exports as a whole. Agri-food products account for the bulk of organic exports (81% of the total) while wine comprises the remaining 19% (a larger share than for Italian agri-food exports in general). This data was obtained from a direct survey of companies – interviewed by Nomisma for Agenzia ICE and FederBio as part of the ITA.BIO pro ect – the only tool available for estimating this important part of the market due to the lack of customs codes that provide an accurate and constant identification of the trade flows of Italian organic products on international markets.

Organic products: characteristics sought by Italians

In 2023, according to the last consumer survey, implemented by Nomisma 90% of population aged 18 and 65 years old claimed to have consciously purchased at least one organic food product in the last year. Indeed, this is an important indicator of the consumer base of organic products and the high level of interest.

The shopping cart composition is becoming more and more complex, reflecting the adoption of different eating styles: 86% of conscious buyers indicate that they opt for 100% plant-based products, 55% purchase “free-from” products (64% lactose-free, 45% gluten-free), while one out of 3 Italian purchased “rich-in proteins” products.

The interest in other product characteristics has determined the orientation of organic product producers, which to date focus much of their offering in the large-scale retail sector on products with Italian origin (34.5% of the references in the organic category) and “rich in” (23.5% with higher shares related to products that are rich in fiber 14.2%, or whole grain 7.8%, than protein – 5.3% which remains the area of greatest development of conventional products).

In addition, organic is still the first choice for most buyers (58%), especially for some categories such as fresh fruits and vegetables, eggs (12 %) and extra virgin olive oil.

But what are the main motivations for Italian consumers to buy organic products First of all, 27% of Italian consumers consider organic products to be safer for health than the conventional option, but also because they are sustainable (23% consider them to be more environmentally friendly, 10% consider them to be more animal welfare friendly, and an additional 10% refer to social sustainability and intend to support small producers).

The importance of knowledge and the role of education

The monitoring conducted by Nomisma clearly highlights some key areas of work that needs to be done for the category, consistent with the sustainability goals of Agenda 2030 – with particular reference to Goal 12.8, which aims by 2030 to enable all people, everywhere in the world, to access relevant information and acquire right awareness of sustainable development and a lifestyle in harmony with nature.

In this logic, the need for improved consumer knowledge has been directly expressed by consumers: in the Nomisma survey 28% believe they do not have enough information to evaluate organic products characteristics, and an additional 57%, despite having good product awareness, would still like to have more information.

The need for more information on the characteristics of organic products and the guarantees underlying certification covers many aspects. First of all, consumers need more information to understand the differences between organic and conventional products (85% of respondents), the sustainability profile linked to the organic production method (72%), and the concrete advantages of the organic method for the environment (75%).

In this regard, the ma ority of consumers who had the opportunity to participate in point-of-sale initiatives felt that the information and communication activities were useful for learning more about the characteristics and guarantees offered by organic brands. In particular, 98% of Italians found the initiative to be helpful in better understanding the differences between organic and conventional products, while 88% were able to understand the guarantees offered by the brand.

Source: Nomisma Press Office